.svg)

How to Finance Your Amazon Business?

Download Amazon Seller Guide

This guide will help you get started, understand the basics of Amazon selling, and explain in simple words how it all works.

Financing an Amazon business is one of the biggest challenges resellers face, especially when scaling operations. Whether you're running a reselling business model (wholesale or online arbitrage), purchasing inventory requires upfront capital, and cash flow can get tight while waiting for Amazon payouts.

Most sellers rely on self-funding to get started – according to Jungle Scout, 81% of Amazon sellers bootstrap their business using personal savings. However, as inventory needs grow, many turn to external Amazon business financing options like credit cards (23%), personal loans (10%), business loans (7%), and Amazon Lending (4%).

The right funding strategy can help you buy more inventory, scale faster, and take advantage of profitable deals. In this post, we’ll explore the best financing options for Amazon sellers, so you can keep your cash flow healthy while growing your business.

What Is Amazon Business Financing?

Amazon business financing refers to the various funding options available to Amazon sellers to help them purchase inventory, manage cash flow, and scale operations. Since selling on Amazon – especially through wholesale and online arbitrage – requires upfront capital, financing solutions allow sellers to maintain a steady supply of profitable products without depleting their personal funds.

Unlike traditional retail businesses, Amazon sellers often face cash flow challenges due to Amazon’s bi-weekly payout schedule and the need to invest in large inventory purchases before generating revenue. This is where business financing comes in–it provides access to capital that sellers can use to buy inventory, take advantage of bulk discounts, and expand their operations.

How does Amazon business financing work?

Amazon business financing works by providing sellers with capital upfront, which is then repaid through fixed monthly payments, revenue-based repayments, or flexible credit lines. The repayment structure depends on the type of financing chosen.

Some common financing options include:

- Amazon Lending

Amazon’s invitation-only loan program for high-performing sellers.

- Business loans and lines of credit

Traditional loans from banks or alternative online lenders.

- Inventory financing and purchase order loans

Loans secured against future inventory purchases.

- Trade credit from suppliers

Wholesale distributors offering net-30 or net-60 payment terms.

- Revenue-based financing

Funding models like Payability, where repayments are tied to sales revenue

- Fintech and peer-to-peer lending

Funding solutions from financial technology companies like 8fig and AccrueMe.

Each financing method has its own advantages, interest rates, and eligibility requirements. Choosing the right one depends on your business needs, financial health, and growth goals. In the next sections, we’ll break down each option in detail and help you determine the best financing strategy for your Amazon business.

Why Amazon Sellers Need Financing

For Amazon resellers, success depends on quick inventory turnover, seizing time-sensitive deals, and managing fluctuating cash flow. Unlike private label sellers who focus on marketing and branding, resellers must continuously reinvest in inventory to maintain momentum and scale. This creates unique financial challenges that require strategic funding solutions to keep operations running smoothly and profitably.

The need for speed: rapid inventory turnover and cash flow cycles

Amazon sellers rely on the velocity of cash flow – the faster they can buy, list, and sell products, the greater their profit potential. However, since inventory purchases require upfront capital and Amazon's payout cycle can delay funds, sellers need readily available financing to keep stock moving. Understanding inventory turnover rates and planning funding accordingly ensures that cash isn’t tied up for too long, allowing for smoother reinvestment and growth.

Capitalizing on limited-time deals and bulk discounts

Resellers frequently encounter time-sensitive deals, such as clearance sales, liquidation opportunities, or bulk discounts from distributors.

These deals can significantly increase profit margins, but delays in securing financing can cause sellers to miss out on lucrative inventory. Having access to business credit, inventory financing, or supplier trade credit allows resellers to act quickly, secure inventory at the best prices, and maximize profits.

Managing cash flow in a volatile market

Reselling on Amazon means navigating seasonal demand shifts, market trends, and competitive pricing changes. Sales can fluctuate drastically, creating potential cash flow gaps that make it difficult to pay suppliers on time or cover operating expenses.

By leveraging financing options such as Amazon Lending, business credit lines, or revenue-based funding, resellers can maintain a financial cushion that allows them to stock up during low-price periods and sustain operations during slow sales cycles.

Scaling a reselling business: the financial challenge of growth

As resellers expand, they need to increase inventory purchasing power, optimize storage solutions, and streamline fulfillment. Growth requires capital investment – whether it’s buying larger wholesale orders, renting warehouse space, or automating logistics.

Financing solutions tailored for scaling, such as business loans, lines of credit, or supplier payment terms, help resellers expand their SKU offerings, manage larger inventory volumes, and build a more efficient operation.

Balancing risk and return: smart financing strategies

Not all financing options are created equal–some come with high-interest rates, strict repayment terms, or hidden fees. Resellers must evaluate their financing choices carefully, considering interest costs, repayment flexibility, and ROI on inventory purchases.

By choosing the right mix of funding sources – such as self-funding, business loans, credit cards, and alternative financing – resellers can ensure they have the capital needed to grow without overleveraging or falling into cash flow traps.

What Are the Funding Options for Amazon Sellers?

Financing an Amazon business requires the right mix of self-funding and external financing to maintain cash flow and scale efficiently.

While many sellers start by reinvesting profits or using personal savings, options like business loans, credit lines, inventory financing, and Amazon-specific funding programs can provide the capital needed to grow without financial strain.

Self-funding your reselling business

Many Amazon resellers start their businesses using their own money–a method known as self-funding or bootstrapping. This approach allows for full control over finances without the burden of interest rates or debt repayments. However, while self-funding works well for beginners, it can also limit growth if cash flow becomes too tight. Below are the most common ways resellers fund their businesses with personal capital and how to do it effectively.

Reinvesting profits: Scaling gradually without debt

One of the safest ways to finance your Amazon business is by reinvesting your profits. As you generate sales, instead of withdrawing earnings for personal use, you put that money back into inventory purchases. This strategy allows for steady growth without financial risk, but it requires patience.

- Advantages

No interest payments, full control over capital, lower financial risk.

- Challenges

Slow growth, limited purchasing power for bulk inventory deals.

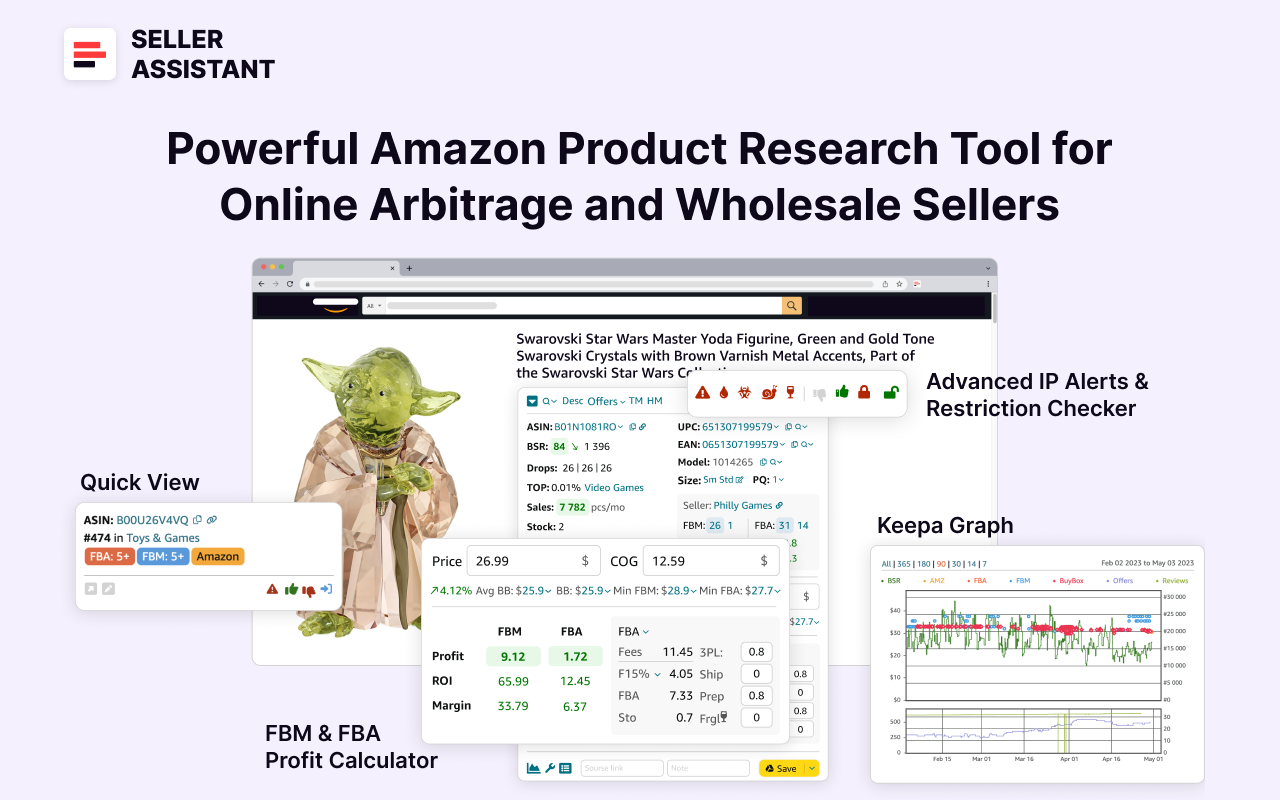

Tip. The key here is to accelerate the reinvestment cycle. The faster you can sell, the faster you can reinvest. When you do product research, focus on fast-moving products. Seller Assistant Extension shows you a product sales velocity (Top %) on the Amazon product pages. If Top is less than 1% (the less the better), the product moves ok. 0.5% and less means a product is a fast-mover.

Note. Seller Assistant is all-in-one product-sourcing software offering 20+ tools that helps Amazon sellers quickly find profitable and low-risk deals. It provides you with effective solutions for bulk wholesale price list scanning and brand analysis alongside advanced product research extensions, tools, and features providing you with in-depth product research data.

It combines three extensions: Seller Assistant Browser Extension, and IP-Alert Chrome Extension by Seller Assistant, and VPN by Seller Assistant, Amazon seller tools: Price List Analyzer, Brand Analyzer, Seller Spy, Bulk Restrictions Checker, and API integrations, and features: Side Panel View, Storefront Widget. Quick View, FBM&FBA Profit Calculator, Sales Estimator, Offers, Variation Viewer, Stock Checker, and offers secure and efficient solutions for teamwork.

Using personal savings: A risky but flexible option

Many new Amazon sellers dip into personal savings to fund their initial inventory purchases. This provides instant access to capital without debt, but it can be risky if personal funds run low.

- Advantages

No credit checks or loan applications, no repayment obligations.

- Challenges

Ties up personal financial resources, potential strain on emergency savings.

Tip. If using savings, treat your business as an investment – set a budget limit so you don’t overextend yourself. Carefully calculate the potential ROI (Return on Investment) of each deal with Seller Assistant Extension. Enter COG (product price at the supplier) and logistics costs. And the tool will show deal ROI.

Using business revenue wisely: Balancing growth and expenses

As your reselling business grows, managing cash flow effectively becomes crucial. This means not only reinvesting in inventory but also ensuring you have enough funds for Amazon fees, shipping costs, and unexpected expenses.

- Advantages

Sustainable long-term growth, avoids reliance on external financing.

- Challenges

Cash flow shortages can slow down expansion.

Tip. Use accounting tools like Sellerboard to track profits and expenses. Set aside a cash reserve to handle slow sales periods.

Business loans for Amazon sellers

For resellers looking to scale faster and manage cash flow gaps, business loans provide flexible access to capital without tying up personal savings. Unlike self-funding, loans allow sellers to buy inventory in bulk, expand operations, and take advantage of time-sensitive deals without waiting for Amazon payouts.

Various traditional and alternative lenders offer funding specifically tailored to e-commerce businesses.

Traditional bank loans: Low-interest but harder to qualify for

Traditional banks offer business term loans and lines of credit with low interest rates and long repayment terms. However, these loans usually require strong credit history, financial statements, and a registered business.

- Advantages

Lower interest rates, structured repayment plans, potential for large loan amounts.

- Challenges

Lengthy approval process, strict qualification requirements, requires good credit.

Example 1. Wells Fargo Small Business Loan

- Loan Amount: $10,000 - $100,000

- Interest Rate: Starting at 7% APR

- Repayment Term: 1-5 years

- Requirements: Credit score of 680+, business must be operating for at least 2 years

Example 2. Chase Business Term Loan

- Loan Amount: $5,000 - $500,000

- Interest Rate: Variable, starting at 6.25% APR

- Repayment Term: 12-84 months

- Requirements: Good credit score, at least 2 years in business, strong financials

Alternative online lenders: Faster approval with flexible requirements

For resellers who don’t meet strict bank loan criteria, alternative lenders offer quick funding options with more lenient requirements. These lenders focus on business revenue instead of credit scores, making them ideal for newer Amazon sellers.

- Advantages

Fast approval, minimal paperwork, tailored for e-commerce businesses.

- Challenges

Higher interest rates, shorter repayment terms.

Example 1. Viably

- Loan Amount: $10,000 - $250,000

- Interest Rate: Custom, based on business cash flow

- Repayment Term: Flexible, revenue-based

- Requirements: Amazon or e-commerce seller with consistent sales history

Example 2. OnDeck

- Loan Amount: $5,000 - $250,000

- Interest Rate: 9% - 50% APR

- Repayment Term: 3-24 months

- Requirements: $100,000+ annual revenue, 600+ credit score, 1+ year in business

Revenue-based financing: Pay as you earn

Revenue-based financing allows sellers to repay loans based on their sales volume instead of fixed monthly payments. This is useful for resellers with seasonal sales fluctuations, as repayments are lower during slow periods.

- Advantages

No fixed payments, funding based on sales performance, works well for seasonal sellers.

- Challenges

Percentage of revenue deducted regularly, which reduces daily cash flow.

Example 1. 8fig

- Loan Amount: Up to $500,000

- Interest Rate: Custom repayment plans (not fixed APR)

- Repayment: Based on revenue share agreement

- Requirements: Amazon or e-commerce seller with consistent sales history

Example 2. SellersFi

- Loan Amount: Up to $5 million

- Interest Rate: Varies, revenue-based repayment

- Repayment: Repay as a percentage of sales

- Requirements: Amazon sellers with strong revenue history

Amazon Lending: Amazon’s own loan program

Amazon offers in-house financing for eligible sellers through Amazon Lending, providing term loans and lines of credit based on sales performance rather than credit history. However, these loans are invitation-only and typically not available for new sellers.

- Advantages

No credit check, competitive interest rates, easy to apply if eligible.

- Challenges

Only available to select sellers, limited loan flexibility.

Loan Types Offered by Amazon Lending

- Term Loans

- Fixed monthly repayments.

- Interest-Only Loans

Lower payments initially, full balance due later.

- Business Lines of Credit

Access to revolving funds as needed.

Example 1. Amazon Lending (by Amazon)

- Loan Amount: $1,000 - $750,000

- Interest Rate: Varies based on seller performance

- Repayment Term: 3-12 months

- Requirements: Invitation-only, based on sales volume

Example 2. Marcus by Goldman Sachs (Amazon Partnership)

- Loan Amount: Up to $75,000

- Interest Rate: Fixed APR (based on creditworthiness)

- Repayment Term: 12-48 months

- Requirements: Amazon sellers with good credit and strong sales history

Credit cards and business lines of credit

For Amazon sellers looking for flexible short-term financing, credit cards and business lines of credit provide on-demand access to capital without the rigid repayment schedules of traditional loans.

These options allow sellers to cover inventory purchases, bridge cash flow gaps, and take advantage of time-sensitive deals while maintaining financial flexibility. Unlike loans, credit cards and lines of credit revolve, meaning sellers can borrow, repay, and borrow again as needed.

Business credit cards: Flexible financing with rewards

Business credit cards are a popular financing tool for Amazon resellers, offering cashback, rewards, and 0% introductory APR periods that help sellers manage expenses efficiently. Unlike loans, credit cards provide immediate purchasing power, making them ideal for smaller inventory purchases, operational costs, and emergency expenses.

- Advantages

Fast approval, earns rewards or cashback, no fixed repayment terms.

- Challenges

High-interest rates if not paid off monthly, potential impact on credit utilization.

Example 1. Chase Ink Business Unlimited®

- Credit Limit: Varies based on business profile

- Interest Rate: 0% APR for 12 months, then 16.24%-22.24%

- Rewards: 1.5% cashback on all purchases

- Requirements: Good credit score (690+ recommended)

Example 2. American Express Blue Business Plus

- Credit Limit: Flexible spending limit based on usage

- Interest Rate: 0% APR for 12 months, then 18.49%-26.49%

- Rewards: 2X points on first $50,000 in purchases per year

- Requirements: Good credit score, business financials may be required

Business lines of credit: Borrow only what you need

A business line of credit works similarly to a credit card but with higher limits and lower interest rates. Sellers can withdraw funds as needed, only paying interest on the amount used. This makes it an excellent option for covering large inventory purchases or managing seasonal cash flow fluctuations.

- Advantages

Only pay interest on what you use, higher credit limits than credit cards.

- Challenges

Variable interest rates, requires business financials for approval.

Example 1. Fundbox Business Line of Credit

- Credit Limit: $1,000 - $150,000

- Interest Rate: 4.66% per draw (varies by creditworthiness)

- Repayment Term: 12-24 weeks per draw

- Requirements: $100,000+ in annual revenue, 6+ months in business

Example 2. BlueVine Business Line of Credit

- Credit Limit: Up to $250,000

- Interest Rate: Prime rate + 1.7% (varies by credit profile)

- Repayment Term: 6-12 months

- Requirements: $40,000+ in monthly revenue, 600+ credit score, 6+ months in business

Choosing between credit cards and business lines of credit

The right option depends on how you plan to use the funds:

- Use a business credit card for smaller, ongoing expenses, taking advantage of rewards, cashback, and 0% APR periods.

- Use a business line of credit for larger inventory purchases or emergency cash flow needs, as it offers higher limits and lower interest rates than credit cards.

Both options provide flexible, revolving access to capital, making them essential tools for Amazon sellers who need fast, adaptable financing.

Amazon-specific funding options

Amazon provides its own financing solutions designed specifically for sellers who need capital to purchase inventory, manage cash flow, and scale their business.

These funding options are often based on a seller’s performance metrics and sales history, rather than traditional credit scores. While Amazon-specific financing can be convenient and tailored to e-commerce businesses, it is not available to all sellers and often comes with limited flexibility compared to other funding sources.

Amazon Lending: Invitation-only financing for sellers

Amazon Lending offers term loans, interest-only loans, and business lines of credit to eligible sellers based on their sales performance. This option is best for established Amazon resellers who need capital to scale but want to avoid traditional loan applications.

- Advantages

No credit check required, competitive interest rates, fast approval.

- Challenges

Invitation-only, limited loan flexibility, funds can only be used for Amazon-related expenses.

Amazon Payability: Daily payouts instead of bi-weekly disbursements

Amazon pays sellers every two weeks, which can create cash flow gaps for resellers who need funds for daily operations. Payability offers instant daily payouts, allowing sellers to access up to 80% of their previous day’s sales.

- Advantages

No credit check, instant access to funds, improves cash flow.

- Challenges

Higher fees compared to traditional loans, reduces daily revenue.

Amazon Seller Wallet: Faster access to Amazon earnings

Amazon Seller Wallet allows sellers to store and transfer their earnings directly within their Amazon account, providing faster access to their funds. This service is designed to help sellers manage their cash flow without relying on external banks.

- Advantages

Quick access to Amazon earnings, simplifies payments for Amazon-related expenses.

- Challenges

Limited functionality compared to third-party payment processors, not yet available to all sellers.

Amazon Business Line of Credit: Revolving credit for sellers

Amazon, in partnership with banks like Goldman Sachs, offers a revolving Business line of credit to eligible sellers. This allows sellers to borrow, repay, and borrow again as needed, making it a great alternative to lump-sum loans.

- Advantages

Flexible funding, no need to reapply for new loans, designed for Amazon sellers.

- Challenges

Invitation-only, repayment terms may vary, not available to new sellers.

Crowdfunding and investor-based funding

For Amazon resellers looking for alternative ways to finance their business, crowdfunding and investor-based funding provide opportunities to raise capital without traditional loans.

These options work best for sellers who have strong business potential but may not qualify for conventional financing. While crowdfunding relies on public contributions, investor-based funding requires sellers to exchange equity or future revenue for capital.

Crowdfunding: Raising capital from backers

Crowdfunding allows Amazon sellers to secure funding from a large group of people who contribute small amounts of money. While this method is more common for private-label product launches, resellers can also use it to finance bulk inventory purchases or business expansion.

- Advantages

No debt, no credit check, potential for viral exposure.

- Challenges

Requires strong marketing, no guarantee of funding, often works better for unique products.

Example 1. Kickstarter

- Funding Model: All-or-nothing (must reach funding goal to receive money)

- Funding Amount: Varies by campaign, no set limits

- Fees: 5% platform fee + payment processing fees (~3-5%)

- Requirements: Campaign approval, detailed funding goal, clear business purpose

Example 2. Indiegogo

- Funding Model: Flexible (receive funds even if goal isn’t met) or Fixed (all-or-nothing)

- Funding Amount: Varies by campaign

- Fees: 5% platform fee + transaction fees (~3%)

- Requirements: Transparent project plan, campaign approval, promotional efforts

Angel investors and venture capital: Selling equity for growth

For sellers planning to scale significantly, angel investors or venture capital firms can provide large amounts of funding in exchange for equity. This option is ideal for resellers looking to expand into new markets or launch additional sales channels beyond Amazon.

- Advantages

- Large capital investments, strategic mentorship, no loan repayments.

- Challenges

- Loss of business control, investor expectations, long negotiation process.

Example 1. AngelList

- Funding Model: Equity-based investment from angel investors

- Investment Amount: Varies by investor, can range from $10,000 - $1M+

- Fees: No direct fees, but investors may take equity

- Requirements: Pitch deck, strong business model, investor networking

Example 2. Crunchbase

- Funding Model: Investor matching and venture capital tracking

- Investment Amount: Varies based on VC firm or investor interest

- Fees: Subscription-based for detailed investor access

- Requirements: Scalable business model, clear growth strategy, investor outreach

Revenue-based financing

Revenue-based financing (RBF) allows Amazon sellers to receive upfront capital and repay it as a percentage of their future sales. This model is particularly useful for resellers with fluctuating revenue or seasonal sales cycles, as repayments are tied to sales performance rather than fixed amounts.

- Advantages

No fixed payments, flexible repayment terms, no loss of equity.

- Challenges

Percentage of revenue deducted regularly, reducing daily cash flow.

Inventory financing: Using inventory as collateral

Inventory financing allows sellers to borrow money using their existing inventory as collateral. Lenders provide funds based on the value of the inventory, and sellers repay the loan as they sell products. This type of financing is useful for wholesalers and online arbitrage sellers who need to stock up before peak seasons.

- Advantages

No need for personal credit, funding based on inventory value, scalable financing.

- Challenges

If inventory doesn’t sell as expected, repayments may become difficult, potential high interest rates.

Example 1. Kickfurther

- Funding Model: Crowdfunded inventory financing

- Loan Amount: Varies based on inventory needs

- Interest Rate: Varies, typically lower than traditional loans

- Repayment: Based on sales performance

- Requirements: Strong sales history, inventory-based business model

Example 2. SellersFi

- Funding Model: Inventory-based loans for Amazon and e-commerce sellers

- Loan Amount: Up to $5 million

- Interest Rate: Varies based on inventory value

- Repayment: Flexible terms based on sales projections

- Requirements: Amazon seller with consistent revenue and inventory turnover

Purchase order loans: Financing bulk orders

Purchase order (PO) financing provides funding to pay suppliers for large inventory orders before a seller receives payment from Amazon. This is useful for resellers who find high-demand products at a discount but don’t have the cash to buy in bulk. The lender pays the supplier directly, and the seller repays the loan after making sales.

- Advantages

Helps secure bulk deals, funding is tied to confirmed purchase orders, good for rapid growth.

- Challenges

Requires verified purchase orders, may have high fees, must manage cash flow carefully.

Example 1. Behalf

- Funding Model: Short-term purchase order financing

- Loan Amount: Up to $500,000

- Interest Rate: Starts at 1% per month

- Repayment: Custom payment schedules based on supplier invoices

- Requirements: Purchase orders from verified suppliers

Example 2. Kickpay

- Funding Model: Automated purchase order financing for e-commerce

- Loan Amount: Varies based on PO value

- Interest Rate: Dynamic based on sales performance

- Repayment: Based on sales revenue or fixed payment plans

- Requirements: Purchase orders from approved wholesalers or suppliers

Choosing the Right Financing Option for Your Amazon Business

If you already have inventory and need to free up cash, inventory financing can provide liquidity without selling off stock. If you need funding for a large wholesale purchase, purchase order financing may be the best option.

Both solutions allow Amazon sellers to buy more inventory without tying up personal funds, making them valuable tools for scaling a reselling business.

In the next section, we’ll discuss grants and government programs, which offer funding opportunities without requiring repayment.

Choosing the right financing option

With so many funding options available, selecting the right one for your Amazon reselling business depends on your financial needs, business stage, and growth goals. Some financing methods offer quick access to cash, while others provide long-term scalability with lower costs. To make the best decision, consider factors like interest rates, repayment terms, flexibility, and risk level.

Assessing your financing needs

Before choosing a funding option, determine why you need financing and how much capital you require.

- Short-term needs (cash flow gaps, quick inventory restock, time-sensitive deals): Business credit cards, lines of credit, Amazon Payability, or revenue-based financing.

- Long-term growth (bulk inventory purchases, warehouse expansion, scaling operations): Business loans, inventory financing, or purchase order loans.

Tip. Always calculate your return on investment (ROI) before taking on debt. Ensure the financing will generate more profit than it costs.

Comparing financing options

Understanding costs and risks

Financing always comes with costs, whether it's interest rates, transaction fees, or equity loss.

What to consider

- How much will the financing cost?

APR, fees, revenue share

- How flexible are the repayment terms?

Fixed vs. variable payments

- What happens if sales slow down?

Can you still meet payments?

- Will it affect your business operations?

Cash flow impact, inventory risks

Tip. Read the fine print. Some financing options have hidden fees or penalties for early repayment.

Making the final decision

Once you understand your needs and the costs involved, choose the financing option that aligns with your business model, repayment ability, and risk tolerance. Here’s how to evaluate the best fit for your Amazon reselling business.

Matches your business model

If you're a wholesaler buying in bulk, inventory financing or purchase order loans may be the best option. If you operate in online arbitrage with frequent smaller purchases, business credit cards or revenue-based financing might be more suitable.

Has manageable repayment terms

Consider how repayment terms will impact your cash flow. Fixed monthly payments from a traditional loan may work well for stable businesses, while revenue-based financing or credit lines offer flexibility for those with fluctuating sales.

Provides the right amount of funding

Taking too little funding may leave you unable to scale or take advantage of deals, while borrowing too much could result in unnecessary debt and high-interest costs. Calculate exactly how much you need based on inventory turnover and expected profits.

Doesn’t put your business at unnecessary risk

Some financing options, like investor funding or high-interest loans, can introduce long-term financial obligations or loss of control. Weigh the risks of each financing choice and ensure you can meet repayment commitments even in slower sales months.

FAQ

How to fund an Amazon business?

Amazon sellers can fund their business through self-funding, business loans, credit lines, revenue-based financing, or inventory-specific funding. The best option depends on factors like business size, growth goals, and cash flow needs.

Is there a way to finance on Amazon?

Yes, Amazon offers Amazon Lending, which provides term loans, interest-only loans, and business lines of credit to eligible sellers based on their sales performance. Additionally, sellers can use Amazon Payability to receive daily payouts instead of bi-weekly disbursements.

What types of financing are available to Amazon sellers?

Amazon sellers can access traditional business loans, credit cards, lines of credit, inventory financing, purchase order loans, crowdfunding, and investor-based funding. Some sellers may also qualify for Amazon-specific funding programs like Amazon Lending or Payability.

Will Amazon give you a loan?

Amazon provides loans through Amazon Lending, but it is an invitation-only program available to sellers with consistent sales and strong performance metrics. If you are eligible, you will see an offer in Seller Central, but if not, alternative financing options may be needed.

Final Thoughts

Financing an Amazon reselling business is essential for maintaining inventory flow, scaling operations, and managing cash flow effectively. Whether you're a wholesale seller or an online arbitrage seller, choosing the right funding option – from self-funding and business loans to Amazon-specific financing and revenue-based funding – can significantly impact your growth and profitability.

The best financing choice depends on your business model, financial stability, and risk tolerance. If you need flexibility, credit lines or revenue-based financing may be ideal, while larger inventory purchases may require business loans or purchase order financing. Amazon Lending and Payability offer seller-specific funding, but they’re not available to everyone, so exploring alternative lenders, grants, or crowdfunding may be necessary.

No matter which financing route you choose, you must select your products to sell wisely with the right product sourcing tools.

Seller Assistant is an all-in-one product sourcing software offering all the features vital for product sourcing. It combines three extensions: Seller Assistant Extension, IP Alert, and VPN by Seller Assistant, tools: Price List Analyzer, Seller Spy, Bulk Restrictions Checker, and API integrations, and features: Side Panel View, FBM&FBA Profit Calculator, Quick View, ASIN Grabber, UPC/EAN to ASIN converter, Stock Checker, and other features that help quickly find high-profit deals. Seller Assistant also offers integration with Zapier allowing to create custom product sourcing workflows.